Tags

The thing about bubble tops is that usually at the time, the media and most of the public are caught up in the euphoria, and only a few voices in the wilderness talk of bubbles. I remember 1999-2000, and 2005-2006. Ordinary cocktail party chatter was about how everyone was getting rich, and most people couldn’t conceive of the bubbly asset going against them. The biggest fear was the fear of missing out. “You can’t lose owning your own home” was a commonplace meme I heard more than once from ordinary people before the housing bubble popped. Anyone who rented was considered an ignoramus.

I don’t see a whole lot of bubbly price action today except in social media and cloud computing stocks, fine art, and high-end collectibles. Caution is warranted, but that is always part of my approach to investing.

By most accounts the overall stock market is a bit overvalued at around 16 times trailing earnings, unless we are headed into a recession. Most of the increase in stock prices over the last year has been from P/E expansion instead of earnings growth, so further upside could be limited to the rate of earnings growth. Short term we are overbought and sentiment is pretty frothy. A 10% or so correction is overdue.

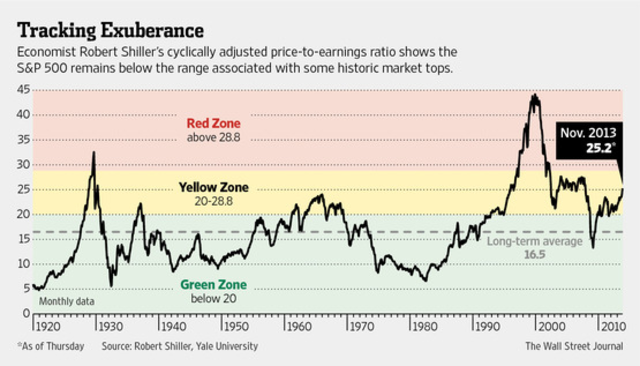

In terms of stock market sentiment among the general public, I still see a lot of skepticism, under-investment, and fear of another crash. Even according to the Shiller cyclically-adjusted price-earnings ratio (CAPE), valuations don’t yet look bubbly. Above average yes; bubbly no.

Some bulls will even argue that the CAPE is distorted by the Financial Crisis, as going forward it isn’t reasonable to expect a credit bubble burst and the resulting hit to earnings every 10 years.

Does any of this mean we can’t have a bear market soon? Nope. The current bull market is about the median length at 4 years and 8 months old from the March 2009 panic low. By this yardstick, one could be just around the corner or 3 – 5 years out. The big question is will we go into a recession or not? Unless some combination of the Obamacare debacle, the Washington debt-default follies, and the Fed taper derail things, economic momentum seems to be slow but steady. Initial jobless claims are at post-crisis lows and this is with the sharp short-term negative impact from the sequester largely moving into the rearview mirror.

Is it time to be wildly bullish? No. That was four years ago when everyone thought the world was coming to an end. Is a bear market on the way? Sure, sometime in the next few years. Is this a bubble top? Likely not. Some — like Ralph Acampora and Jeff Saut — see us in a long-term (secular) bull market. If so, a 20% – 30% pullback would be a good entry point.

What will happen? Nobody knows. Investing isn’t about certainties, it is about subjective probabilities and calculated risk. Blood isn’t running in the streets, so I wouldn’t be putting a ton of new money to work now, but things can work higher from here. Keeping a close eye on your risk level is always a good idea. But without big policy screwups, 2014 could be a good year for the economy. We could also continue the slow grind higher in what Barry Ritholtz has called the most hated bull market of all time.

Video: Bubble Talk is a Lot of Hot Air According to Ritholtz

“Bull-markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” — Sir John Templeton