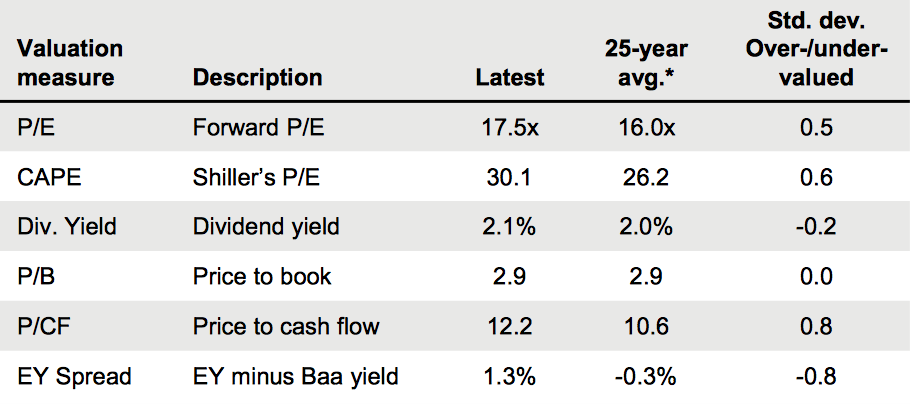

So where do we stand with the stock market? The S&P 500 trades at just under 22 times trailing operating earnings according to Bloomberg …

… and 17.5 times forward earnings estimates according to J.P. Morgan.

So by these measures, the market is overvalued compared to 25 year averages. However, when the earnings yield is compared to current interest rates, the market is — if anything — rather cheap.

Ed Yardeni calls the current conventional wisdom the “2-by-2-by-2” scenario: 2% real GDP growth, 2% inflation, and a peak Fed Funds rate of 2%.

What If We Have Much Higher Interest Rates?

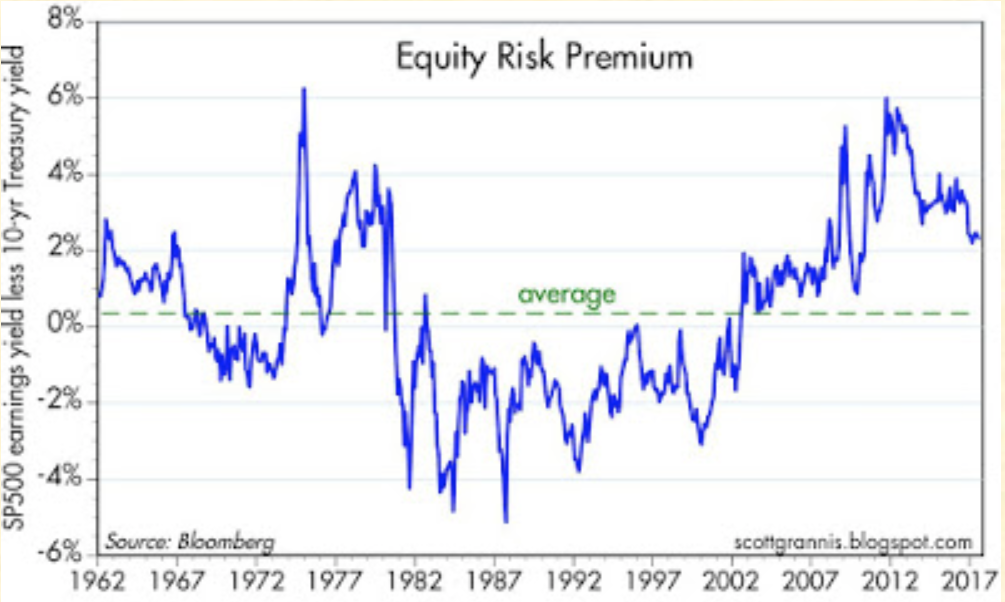

But much higher interest rates could upset the apple cart. While there are many reasons for lower potential growth and inflation — such as the aging of society — what if the conventional wisdom is wrong and higher growth and inflation cause a substantial increase in interest rates?

As the above chart shows, interest rates don’t generally have a negative effect on stocks until the ten year Treasury is above 5%. While it’s not impossible for rates to go higher than 5%, I see no reason for it to happen any time soon without much higher growth and/or inflation rates. And demographics and global trade would seem to keep a lid on both.

Runaway Inflation Seems Rather Unlikely

There are a lot of smart people who seem to think a normalized 4%-5% ten year Treasury yield is a reasonable planning assumption. For instance, Morningstar has a 4-5% ten year Treasury baked into its discounted cash flow (DCF) models to come up with their fair value estimates on stocks.

There is a lot of room between the current 2.24% on the ten year Treasury and a potential 5 handle. But with gradual Fed balance sheet reduction and possible higher growth from a tax cut or infrastructure package, the 10 year Treasury could easily reach 3%-3.5% over the next year or so — maybe even 4%. But that would require the Keystone Cops in Washington to get their acts together. And don’t forget the Fed is pushing in the other direction with higher short term interest rates because their outdated Philips Curve Model suggests inflation should be on its way any day now.

While commodities prices are mixed (weak ag prices/strong industrial metals), global trade should ease pressures on inflation. The official unemployment rate looks low, but there still seems to be some slack in the labor market with the low participation rate and wage growth below par. And to the extent wage pressures exist, companies will likely invest more in automation.

Maybe A Lot More Long Term Upside?

The good folks at Bespoke show that trailing 10 and 20 year stock market returns are still pretty lousy, which hardly seems an indication of a bubble ready to be popped.

And as this chart shows, we may well have entered a new secular bull market in 2013, which could bring huge gains over the next decade plus.

Can The Fed Control Its Urge to Cause a Recession?

So even though we’ve had a great 8 year run since the bottom in March of 2009, it seems we have room to the upside if the economy continues to do well. Unless we have a big geopolitical shock or the Fed hikes us into a recession. If we get a recession, we get a bear market. This is as close to a certainty as you will find in the markets.

While it seems everyone is looking for signs of the bottom falling out of the stock market, the data shows no bubble that I can see. Well, Tesla and Nvidia look rather bubbly but M&A and the IPO market are certainly not red hot. Big Cap Tech has had a great run, but they have real earnings and cash flows, and valuations are much more reasonable than during the bubble era. This is not about metrics like eyeballs and page views like 1999-2000. There is no sock puppet bullshit this time; by and large, they are real, substantial businesses.

It seems to me there is no need for a recession unless the Fed decides it wants to cause one by raising rates too much — so they can get the dry powder to lower rates in case of a recession, which they will likely cause by raising rates…

How To Plan For An Uncertain Future

If you are worried about a bear market, you should reduce your risk while times are good. Make sure you have enough liquidity so you won’t stop buying during a bear market if you are young and in the accumulation phase. And don’t sell into a decline!

Planning for your liquidity needs is even more important if you are in or near retirement. If you are worried about a coming bear market, you should sell down to the sleeping point now, when times are good. Don’t put yourself in a position to be a forced seller into a big decline. That only makes you fail to meet your long term goals while lining the pockets of guys like Warren Buffett and Seth Klarman.

I try to stay hunkered down all the time, and I plan for my liquidity needs as if a bear market will begin tomorrow. This is more sensible than to assume you will have some magical insight nobody else has that will enable you to sidestep the worst of a bear market.

See also:

J.P. Morgan Guide To the Markets as of June 30, 2017

“Run of the Mill” Market Returns – Bespoke

S&P 500 Remains Reasonably Valued – Brian Gilmartin

Jeff Saut Still a Huge Secular Bull

“Success in investing doesn’t correlate with I.Q. once you’re above the level of 125. Once you have ordinary intelligence, what you need is the temperament to control the urges that get other people into trouble in investing.”

— Warren Buffett